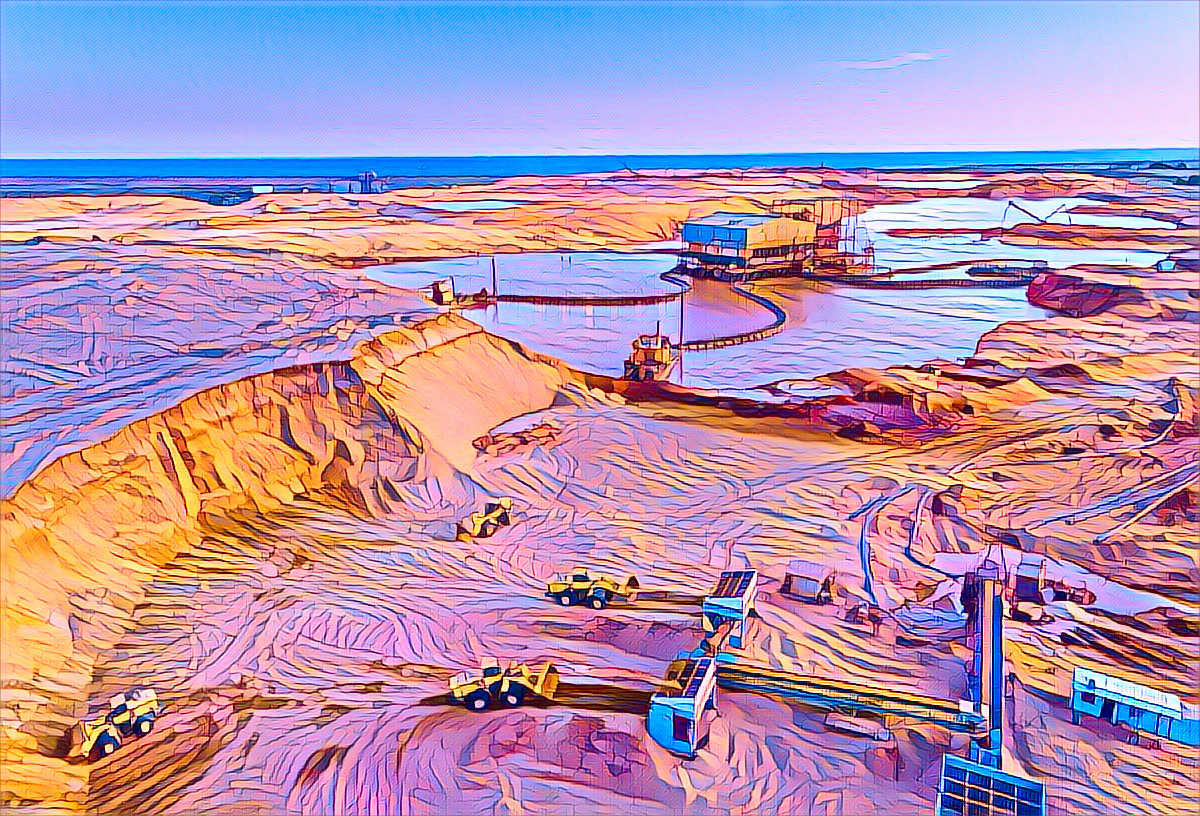

Titanium and zircon producer Kenmare Resources confirmed in a July 17 trading update that it is on track to achieve its full-year guidance for all stated metrics. The company operates the Moma titanium minerals mine in northern Mozambique.

Kenmare MD Michael Carvill highlighted the positive outlook for the second half of the year. “Higher ore grades in the second half are expected to support stronger production, and shipments are also expected to rise. Demand for all of our products remains robust, and ilmenite prices in the first half were above our expectations, bolstered by increasing global pigment production,” he said.

Carvill stated that the company ended the period with $58.5 million in cash, having paid $34.4 million in dividends and repaid all debt. “The company is well-capitalized to fund the upgrade and transition of wet concentrator plant (WCP) A and to continue making shareholder returns,” Carvill added.

Kenmare reported a rolling 12-month lost-time injury frequency rate (LTIFR) of 0.09 per 200,000 hours worked to June 30, a significant improvement from 0.18 in the previous period.

The company produced 342,600 tons of heavy mineral concentrate (HMC) in the second quarter, a 7% increase year-on-year. This was driven by an 8% increase in excavated ore volumes and higher heavy mineral recoveries, which offset a 5% decrease in ore grade.

Ilmenite production rose by 8% year-on-year to 238,600 tons, supported by a 6% increase in HMC processed and greater ilmenite content in the HMC. Primary zircon production increased by 12% year-on-year to 13,000 tons, benefiting from increased HMC processing, intermediate stock drawdown, and higher recoveries.

Total shipments of finished products amounted to 234,700 tons, down 18% year-on-year due to poor weather conditions and additional operational maintenance, which limited shipping time.

Despite the decrease in shipments, the company experienced encouraging market conditions in the second quarter. Strong demand for ilmenite and a robust order book for the third quarter contributed to the positive outlook. By the end of the first half, Kenmare’s net cash increased by $36.4 million to $57.1 million, compared with $20.7 million on December 31, 2023.

Carvill confirmed he would resign from his executive role and board position on August 14. The process to find his successor is approaching its conclusion, with an update expected ahead of the interim results being published.

The company reported a fatality at the Moma mine on June 1, involving an excavator operator employed by one of its contractors. Investigations revealed the incident was related to activities outside the ordinary course of operations. Kenmare is cooperating with authorities.

Finished product output increased by 8% in the second quarter compared to the previous year, mainly due to a 6% rise in HMC processing. Rutile production increased by 32%, supported by intermediate stock drawdown and higher recoveries. Concentrates production grew by 13% to 11,700 tons.

Additional maintenance on the product transfer conveyor system, now fully equipped for increased loadout rates, was required during the quarter. Shipments comprised 216,200 tons of ilmenite, 8,200 tons of primary zircon, and 10,400 tons of concentrates.

The closing stock of HMC at the end of the second quarter was 24,600 tons, compared with 25,300 tons at the end of the first quarter. The closing stock of finished products was 273,000 tons, compared with 241,800 tons at the end of the first quarter, reflecting production exceeding shipments during the quarter.

Kenmare expects stock levels to remain higher than usual in the second half of the year before normalizing in the first half of 2025.

Kenmare’s board approved the final part of the definitive feasibility study (DFS) for the WCP A upgrade and transition to the Nataka orezone, securing production from Moma for decades. The total capital costs for the project remain in line with previous estimates, at $341 million.

Detailed engineering and scheduling work have deferred $38 million of expected capital expenditure from this year into subsequent years. Work is progressing well for the upgrade, including the fabrication of new dredges and the upfront desliming circuit. The detailed design of the tailings storage facility (TSF) is on track for completion in the third quarter.

Kenmare is also working on the DFS for the WCP B upgrade, expected to increase WCP B’s capacity by over 40%, and the prefeasibility study for the Congolone orezone, a potential future growth opportunity.

Kenmare experienced robust demand for all its products in the second quarter, particularly for ilmenite. Spot prices for ilmenite remained stable throughout the first half, although the average received price decreased slightly in the second quarter compared to the first quarter due to some shipments rolling over from the fourth quarter of 2023. Prices in the first half were above the company’s expectations.

Chinese pigment producers continued to produce at record levels. Demand for Kenmare’s ilmenite was bolstered by increased operating rates among pigment producers in Europe and the US.

Global supply of titanium feedstocks remains sufficient to meet demand. New supply from Chinese producers in African countries ships concentrates to China for processing. However, this was partially offset by the suspension of operations in Sierra Leone and continued mineral resource depletion in Kenya.

In the medium to long term, Kenmare expects supply constraints to lead to global demand exceeding supply, supporting the fundamentals for all of the company’s products.

The zircon market remains relatively stable. Demand for zircon sand improved in Europe in the second quarter, particularly from the ceramics industry. In China, the market softened following improvement in late the first quarter. However, Kenmare continues to experience robust demand for its concentrates in China due to the quality of the products it contains.

Kenmare has a strong order book for the third quarter as customers restock their titanium feedstock inventories, following Kenmare’s disrupted shipping performance in the second quarter. Zircon shipments delayed from the second quarter will also be shipped in the third quarter, positively impacting the second-half product mix and revenues.

On May 17, Kenmare paid its 2023 final dividend of $0.3854 per share. This was the balancing payment of a 2023 full-year dividend of $0.5604 per share, representing a dividend payout ratio of 38% of profit after tax in 2022.

Following the 2023 final dividend distribution of $34.4 million and principal debt repayments of $47.1 million during the first half, cash and cash equivalents were $58.5 million on June 30. On December 31, 2023, cash and cash equivalents were $71 million. Kenmare had no debt at the end of the first half.

On December 31, 2023, debt was $50.3 million, and lease liabilities were $1.3 million. On June 30, Kenmare’s net cash had increased by $36.4 million to $57.1 million, compared with $20.7 million on December 31, 2023.

Source: Mining Weekly